SuperTutor

$15/per page/Negotiable

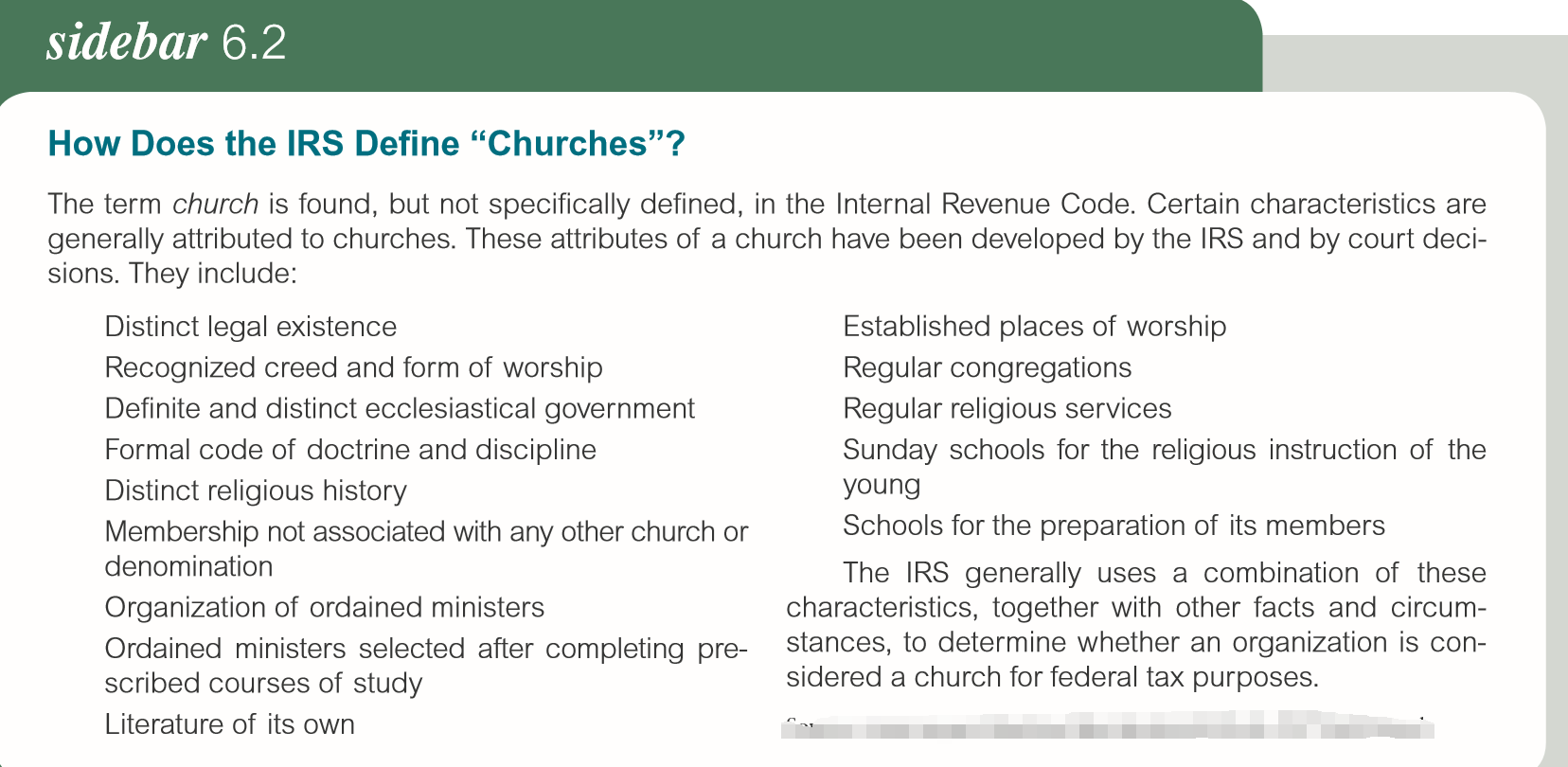

sidebar 6.2 How Does the IRS Define “Churches”? The term church is found, but not specifically defined, in the Internal Revenue Code. Certain characteristics are

generally attributed to churches. These attributes of a church have been developed by the IRS and by court deci-

sions. They include: Distinct legal existence Established places of worship Recognized creed and form of worship Regular congregations Definite and distinct ecclesiastical government Regular religious services Formal code of doctrine and discipline Sunday schools for the religious instruction of the

Distinct religious history YOUNG Membership not associated with any other church or SChOOIS for the preparation 0f its members

denomination The IRS generally uses a combination of these

Organization of ordained ministers characteristics, together with other facts and circum-

Ordained ministers selected after completing pre- stances. to determine whether an organization is con-

scribed courses of study sidered a church for federal tax purposes. Literature of its own *' I I I

{kind=link}